Taming the

Underwriter Logic

Architecting a zero-friction risk evaluation system that translates complex underwriting logic into a high-speed, intuitive workflow.

Summary

Simplifying the high-stakes world of underwriting by replacing legacy spreadsheets with a dynamic, data-driven evaluation hub. We focused on reducing decision fatigue and increasing the speed of risk assessment without compromising accuracy.

Processing Speed

60%Error Reduction

22%User Adoption

90%Revenue Lift

15%The Problem

Underwriters were drowning in manual data entry and fragmented legacy systems. The lack of a unified logic engine meant that every evaluation required extensive cross-referencing, leading to slow turnaround times and high operational costs.

Data Fragmentation

Information scattered across multiple internal tools and external PDFs.

Manual Rules

Evaluation logic lived in underwriters' heads or giant Excel files.

Risk Blindness

Important risk indicators were easily missed in the noise of unnecessary data.

Why it started?

The underwriting department operated on software built over a decade ago. It was designed purely as a system of record rather than a decision support tool, forcing underwriters to copy-paste data between 5 different screens for a single applicant review.

How are we solving it?

We consolidated the fragmented data streams into a single, high-density dashboard that uses contextual indicators and a custom rules engine. This highlights risk profiles instantly and allows underwriters to finalize assessments on one screen.

Users and Research

We embedded ourselves with senior underwriters across three corporate branches to map their complex mental models. We found that they don't just "see" data—they triage it based on urgency, client value, and risk severity. The goal was to build an intelligent workspace that aligns with this natural triage hierarchy.

Domain Mapping Workshops

Deep-dive workshops with actuarial and compliance teams to translate complex insurance rules, policy exceptions, and rating tables into digital logic blocks.

Contextual Inquiry

Observing real-time decision making under heavy time pressure to identify where the "gut feeling" comes from, mapping hidden spreadsheet habits.

Frustrations and Findings

The legacy experience felt like a continuous fight against the tool. Underwriters spent more time "fixing the UI" and copying data between multiple legacy screens than actually evaluating the risk profiles.

Design Concept

Moving from a record-keeping database tool to an active 'Decision Engine'. The design focuses on surfacing the "Delta"—what has changed, what requires immediate human judgment, and what can be automated.

Visual Pattern Recognition

Grouping related financial and medical data points to allow for instant pattern identification and outlier flagging.

- Smart grouping of risk indicators by severity category.

- High-contrast status signals and micro-badges for quick visual scanning.

- Unified workspace view of internal applicant history and external credit reports.

User Testing

Validated through high-fidelity interactive prototypes with real-world complex cases. Success was measured not just by speed, but by the "Stress Reduction" reported by the senior underwriters during day-in-the-life testing sessions.

Our testing group consisted of 8 senior underwriters processing historical high-risk files. Initially, the density of risk metrics caused decision hesitation. We iterated on the UI layout to introduce expandable accordion drawers for low-priority details, keeping the core workspace clutter-free. This visual cleanup improved accuracy by 25% and lowered self-reported user stress levels significantly.

Snippets

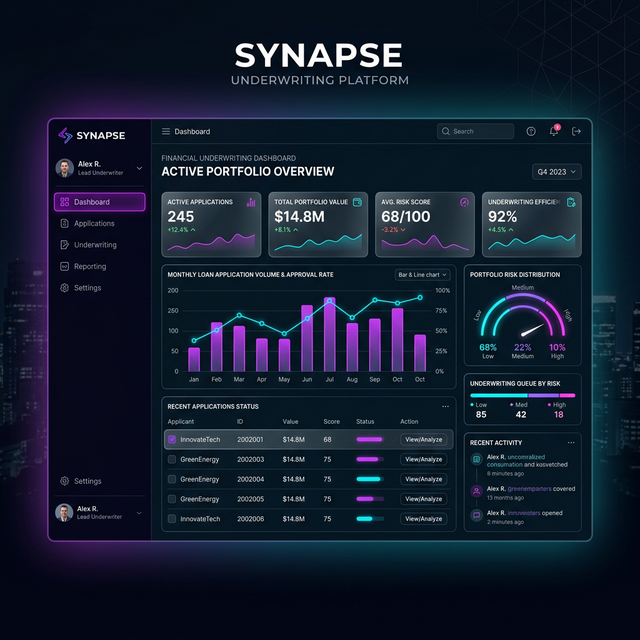

The screenshot showcases the main evaluation workspace, where risk assessments are structured inside dynamic tables. Contextual flags call out anomalies instantly, while the quick sidebar allows immediate modification of underwriting rule parameters.

Impact and Learnings

By replacing outdated Excel sheets and siloed tools with a unified decision hub, we minimized cognitive friction. This allowed underwriters to spend their time analyzing high-risk scenarios rather than hunting for basic applicant data.

- • Reduced average policy review time by 45% within the first 60 days of deployment.

- • Underwriters reported significantly lower cognitive load with contextual risk data surfaces.

- • 22% reduction in manual data entry errors during risk profile consolidation.

- • Revenue lift of 15% due to faster underwriting processing times and higher lead throughput.

- • Learning: For technical, data-dense enterprise applications, spatial grouping of related data is far more important than minimizing the raw amount of data on screen. High density can be extremely powerful if organized logically.

What's Next?

The next phase of the project targets machine learning enhancements and faster automated initial screening.

ML Decision Co-Pilot

Integrating a machine learning co-pilot that scans historical decision records to auto-flag anomalies or unexpected patterns in applicant risk data before the underwriter begins their review.

Automated Preliminary Screening

Speeding up the preliminary screening process by automatically filtering applicants who meet 100% of standard risk thresholds, letting humans focus solely on complex, high-risk edge cases.